Successful Dental Associateship Recruitment

Part 3: Finding the Right Dental Associateship

The American Dental Association reports that about half of all associateships fail (Ebert, n.d.). Other sources paint a more drastic picture, claiming that 8 in 10 associateships dissolve (PTS, 2022). Dental associateship failures emotionally impact the owner, the staff, and the associate, making it harder to trust and try again. While there is no guarantee that you will have a successful hire, there are strategies that can increase your chances of making an excellent match for your office. This segment of our series will examine how to hire, train, and manage an associateship to maximize your chances of success.

Finding the Right Person

In the first two segments of our three-part series, we looked at reasons dentists might hire an associate and how to know if the timing is financially right. When owners have carefully evaluated the reasons for the dental associateship and have calculated their office’s profitability and break-even point, they are ready to begin crafting a job description that can be used to identify the right candidate for their unique situation.

The Research Phase.

The owner dentist seeking to hire an associate must begin by researching best practices in hiring and paying an associate. Owners should thoroughly develop a compensation plan while tailoring the associate’s job description. Some models of compensation per the ADA (n.d.) are as follows:

- Straight Salary: When owners pay a straight salary, payroll calculations are based the total yearly salary divided by the number of payrolls per year or the daily rate times the number of days worked per pay period. For example, if the associate is offered $182,000 annually, paid bi-weekly, the gross or pre-tax pay is $7,000 per pay period.

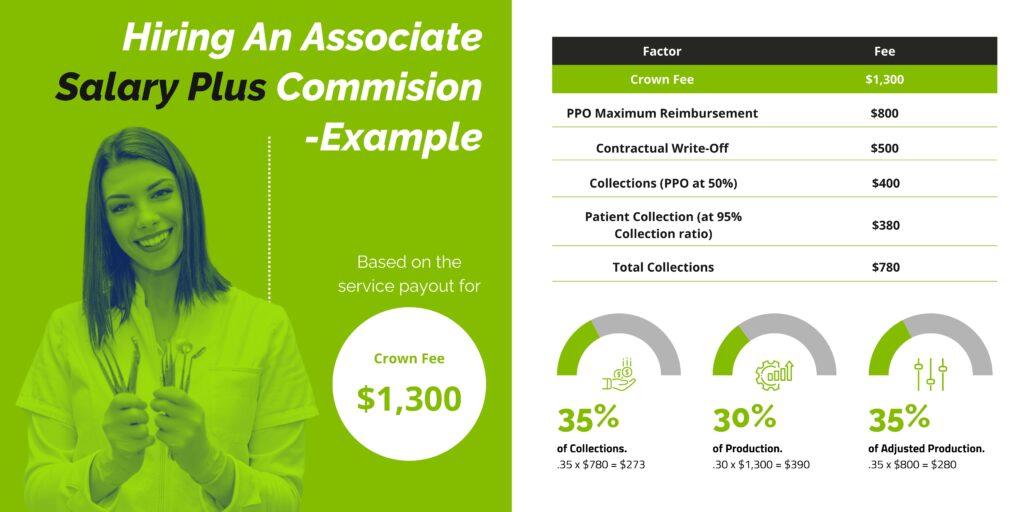

- Salary Plus Commission: Under this structure, the associate would have a guaranteed base salary plus earn extra income based on productivity. For example, in addition to the $7,000 base pay, the associate may earn 10%-30% of their gross production. Suppose the associate produces $40,000 in one month. In addition to the $7,000, the associate would earn an additional $4,000-$12,000.

- Commission: Under this system, associates receive compensation based on a percentage of production, adjusted production, or net collections. An example of paying on commission is provided below.

- Net Profit: This method compensates associates on adjusted production minus a share of the office’s expenses. Typical expenses deducted are the associate’s pro-rata share of laboratory fees and supplies.

When deciding on the associate’s compensation method, remember to stipulate the following:

- How will the associate receive patients?

- Will the associate be allowed to perform all the work they diagnose, or will a more senior dentist do higher-dollar procedures?

- How will contracted insurance reimbursement rates affect the associate’s pay?

- How will hygiene exams factor into compensation?

- How robust is the office’s collection ratio?

- Will the associate have additional compliance or managerial duties?

- What additional benefits, such as health or liability insurance, pension, or continuing education, are part of the total compensation package?

- When and how often will compensation be re-negotiated?

Articulating the compensation method may be the most crucial factor in securing a successful owner-associate relationship. It is essential that neither party feels disadvantaged or trust suffers. It is wise to provide examples for the associate to see how compensation will work in your office. The example below depicts how different commission compensation methods affect an associate’s pay. If associates are paid using another method listed above, adjust the base pay and/or percentages to provide authentic examples based on your unique situation.

Associate Contracts.

Associate contracts are complex documents, so owners should always engage an attorney to write the contract. In addition to compensation, benefits, and perks, the contract should detail working hours, expectations, termination processes, restrictive covenants, contract length and renewal terms (Chelle Law, n.d.).

Worker Classification.

The final compensation decision when adding an associate is determining if the associate will be classified as a W-2 employee or an independent contractor. Owners should not take employee classification lightly since misclassified employees can be costly for the owner and the associate ( Prescott et al., 2017). Owners who misclassify are subject to resolving tax deficiencies, penalties, and interest. Misclassified associates are impacted by self-employment taxes, ineligibility for fringe benefits, and unreimbursed business expenses. Prescott et al. (2017) emphasize that the IRS focuses on the control aspect in its ruling on provider classification (See Revenue Ruling 87-41 for 20 factors that influence the classification of workers). In Dental Economics, Prescott (2017) states the following: “If the practice pays the associate, schedules the associate, requires the associate to follow practice policies, and subjects the associate to a restrictive covenant, the associate is an employee.” Therefore, it is wise to consult a CPA or attorney when making this critical decision.

Crafting a Job Description.

Just as owners might use a job description document for other office roles, they should also list the desired qualifications for an associate. This document should specify the skill sets required, work hours, and office responsibilities. For example, if the new associate will be responsible for all hygiene on a specific day or if they must work some night or weekend hours, list them. Suppose they will be accountable for compliance initiatives within the office or manage certain staff members. In that case, those expectations belong in the job description, too. Beyond these items, however, owners should list values and people skills that the new associate should possess along with any specific personality or work characteristics needed to succeed in the office environment and culture.

This document should encompass the ideal candidate, but no one candidate will measure up to perfection. It may be helpful to order or rank the different characteristics. If certain items are non-negotiable, rank them as such. If others are less critical, indicate that. In this way, owners will formulate a clear picture of what they feel is best for their offices and be able to assess each candidate against the job description. The job description is not a static document. As owners move through the interview process, they may discover areas that need to be added to the description or decide to remove specific requirements that seem less important.

A critical aspect of the job description is identifying the type of associateship offered. Is the owner hoping to hire for an eventual buy-in or buy-out? Is the dental associateship mainly to provide a new revenue stream? Make sure the candidates understand the intention of the hiring. Otherwise, owners may be surprised if the associate has different objectives from their own.

The Interview Process.

Once owners have a clear job description, they can begin developing interview questions for the candidates and envisioning how they will conduct the interviews. Make sure to formulate open-ended interview questions. Yes or no questions rob the interviewer and the candidate of the opportunity to explore intentions and innuendo. Nothing can be worse for either party than to misinterpret answers, so strive to listen well, not just to be polite. Encourage candidates to ask questions of their own. Suggesting that they bring a question set for you to answer may be helpful since the goal of the interview is to discover if both parties want to move forward in the alliance. Uncovering as much information as possible will help everyone make a sound decision.

As the interview progresses, be alert for red flags indicating that the candidate’s goals are divergent or conflicting. Also, avoid asking illegal interview questions about race, gender, religion, age, family status, and other similar demographics. It is also unlawful to ask about citizenship or disabilities. The Great Lakes ADA Center reminds us that the purpose of the interview is to meet the applicant and learn more about their education, credentials, and experience, not to discover if the applicant has a disability or how severe it is. As interviewers relax during the interview, it is not uncommon to over-share about themselves or over-inquire about the candidate. Be vigilant to keep the interview’s tone professional and legal from start to finish.

There is no benefit to hastening the interview process, and setting up multiple back-to-back interviews is inadvisable. Instead, take time to reflect on each candidate’s strengths and weaknesses without the distraction of needing to rush to another interview. Also, be sure to allow trusted staff members to provide their impressions of the candidates. However, it is essential to show respect toward all candidates in front of the staff because one or another candidate will eventually be part of the team.

The Offer and Negotiation Phase.

The offer and negotiation phase is the most crucial part of hiring an associate because it formally sets the stage for how the arrangement will work. Once owners identify the right candidate, they should offer employment. Provide the potential hire with the contract and a written summary of the job expectations, terms of employment, and compensation package. Give the candidate time to think about the offer and consult their counselors. Arrange a suitable meeting time to enter negotiations.

Chelle Law.com (n.d.) emphasizes that a well-negotiated contract can lead to long-term success and job satisfaction. In contrast, a poorly negotiated contract may result in legal disputes and financial strain. Tips for a successful negotiation phase are as follows:

- Negotiate in person to ensure good communication. Body language is a good indicator of how the meeting is proceeding.

- Expect the associate to have questions. It is not a healthy sign for someone to accept the contract without questions or without asking for stipulations.

- Keep a respectful tone during the conversation.

- Be ready to compromise on some terms. Think carefully about any points of challenge to determine if you can adjust the terms on that point.

- Do not rush the negotiation phase to avoid missing important details of the relationship.

- Be prepared to walk away if agreement to terms is not possible.

- Change contract terms with the help of your attorney.

- Expect multiple meetings to conclude negotiations.

Hopefully, the owner’s careful preparation will yield a successful hire and a fulfilling new relationship for both the owner and the associate.

Resources

For more information about appropriate interview questions, see these helpful resources

EEOC: Problematic Questions to Avoid

References

ADA.org (n.d.). Dentist compensation: What every dental associate should know. ada.org/resources/careers/dentist-compensation

Chelle Law (n.d.). Strategies for dental associate contract negotiation. https://www.chellelaw.com/strategies-for-dental-associate-contract-negotiation/

Ebert, J. (n.d.).5 tips to find the right dental associateship for you. 5 Tips to Find the Right Dental Associateship for You | American Dental Association (ada.org)

Prescott, W. P. (2017, June 1). The dental associate contract. https://www.dentaleconomics.com/practice/new-dentists/article/16389554/the-dental-associate-contract

Prescott, W. P., Altieri, M. P., VanDenHaute, K. A., & Tietz, R. I. (2017). Worker classification issues: Generally and in professional practices. Practical Tax Lawyer, 31(2), 17-28. https://www.wickenslaw.com/media/i2of55jt/worker-classification-issues-generally-and-in-professional-practices-1.pdf

PTS (2022, December 12). Why most dental practice associateships fail. Why Most Dental Practice Associateships Fail – Professional Transition Strategies

Yang, K. L. & Tan, H. E. (2024). Pre-employment screening considerations and the ADA. In Disability & HR: Tips for human resources professionals. Institute on Employment and Disability. Cornell University. https://www.hrtips.org/article_1.cfm?b_id=17